Editor’s Note: Overdraft Apps provides detailed product reviews and recommendations based upon extensive research and our own hands-on testing. We may earn a referral fee when you sign up for or purchase products mentioned in this article.

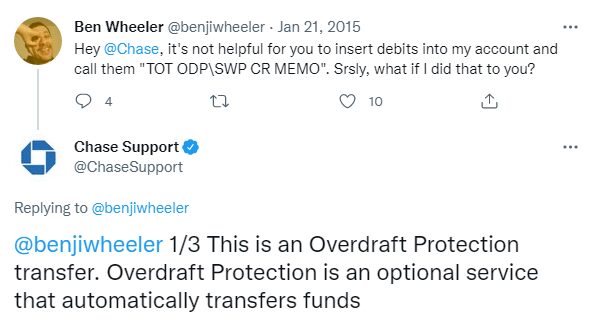

“TOT ODP SWP CR MEMO”

In a world when bills and bank notifications fly from your phone to your laptop and (sometimes still) your mailbox, it’s easy to get lost in endless abbreviations and jargon.

So, what does tot odp swp cr memo mean when it appears on a bank statement, and should you be worried?

We’ll answer that question in the next 30 seconds and tell you *exactly* what you need to do if you spot this charge on your next statement.

Why is Cleo one of our favorite cash advance apps?

- Super speed - Get up to $250 in your bank account today!2

- No, No, No! - No credit check, no interest, no tips, no late fees

- 😂 😂 🤣 - Hilarious, smart money advice you might finally listen to

What we’ll cover:

- What is TOT ODP SWP CR MEMO?

- What does TOT ODP SWP CR MEMO stand for?

- Reasons you’re seeing tot odp swp cr memo on your bank statement

- Be aware of tot odp swp cr memo variations

- What to do if you see a tot odp swp cr memo charge

- Apps to help you avoid Chase Overdraft fees

- Can you get rid of a tot odp swp cr memo charge

- Final thoughts and what to do next…

Need quick cash to avoid costly overdrafts? >>> Compare loans at PockBox

What is TOT ODP\SWP CR MEMO mean?

If you see the following charge on your statement – tot odp/swp cr memo – then it’s a charge relating to overdrafts in your Chase checking account.

If you’ve opted into Chase’s overdraft protection for your checking account and have initiated a transaction that will push your balance negative, then Chase bank will automatically transfer funds from from your linked savings account to your checking account to try to bring the balance back above $0.

TOT ODP SWP CR MEMO is the transaction that shows these funds moving from your checking account to your savings account. You’ll also notice a corresponding transaction for the same amount in your savings account, except this one will be labeled TOT ODP SWP DR MEMO.

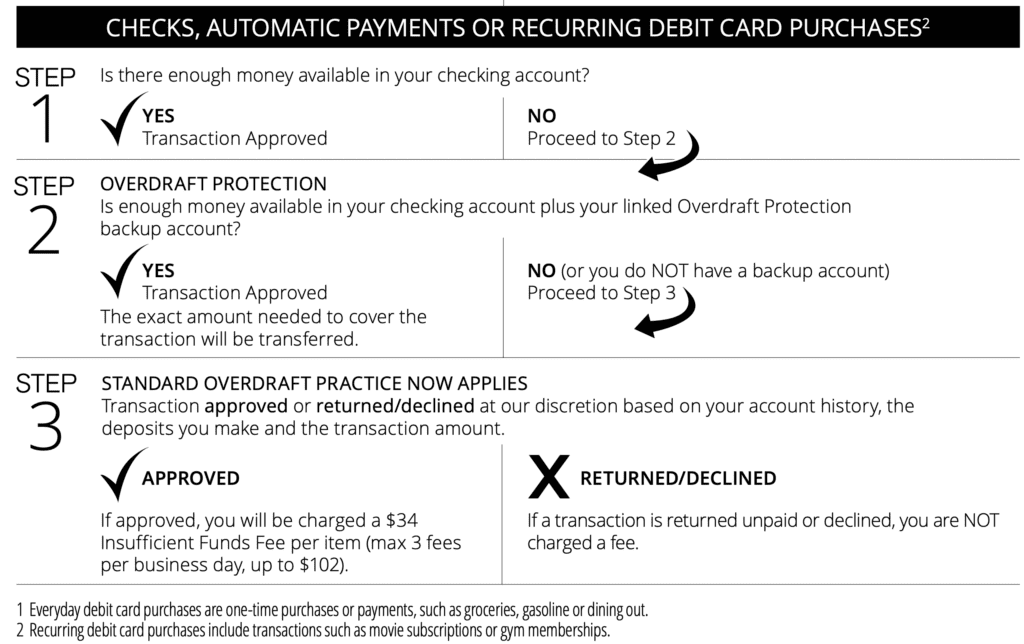

If you have sufficient funds in your linked savings account, this is a pretty straightforward and harmless transaction, though it’s a good idea to replenish your savings account so have funds available for the next time you’re a little short on cash. However, if your savings account balance can’t cover the entire amount of your transactions, things can get a bit frustrating and expensive.

If you’re enrolled in overdraft protection, you can still use your debit card to make purchases, and checks and scheduled bill payments will still be paid (all subject to the bank’s discretion). You won’t be able to withdraw cash from an ATM or bank branch.

And you’re likely to start incurring overdraft fees, which cost $34 each. Chase will charge you for up to three overdrafts per day, which totals a painful $102, especially if it’s for just a few small purchases. The bank is a bit nicer than it used to be, and there are no overdraft fees if your account is less than $50 negative or if you make a purchase for under $5.

What does TOT ODP SWP CR MEMO stand for?

TOT = Temporary Overdraft Transaction

ODP = Overdraft Protection

SWP = Sweep (the bank moving money from one account to another)

CR = Credit (money moved into your account)

MEMO = description of the transaction (though not a very helpful one!)

Reasons you’re seeing tot odp swp cr memo on your bank statement

There are plenty of situations that can cause you to see this overdraft-related charge on your monthly bank statement.

As this financial term relates to overdrafts, you may be paying transfer fees or your account may have been overdrawn as a result of:

- ATM Withdrawals

- Debit Card Purchases

- Checks

- Bill Payments

- Temporary Deposit Hold

- Unexpected Subscription Debits

- Authorization Holds

- Bank Fees

- Funds unavailable due to a debit card hold on a pending transaction

- Memo post for a temporary transaction that reduces your balance

Before we show you how to remove or avoid this charge, it’s important you’re aware of the multiple variations that may appear on your monthly statement.

Be aware of tot odp swp cr memo variations

If you think there are clearer ways to inform you of overdraft fees… you’d probably be right. But Chase uses this, or a variation of this, to let you know your account went into overdraft protection.

You may also see this charge on your statement in one of the following forms:

| Variation #1 | tot odp swp cr memo |

| Variation #2 | tot odp\swp cr memo |

| Variation #3 | tot odp/swp cr memo |

| Variation #4 | tot odp swp dr memo |

| Variation #5 | pending tot odp\swp cr memo |

| Variation #6 | tot odp\swp dr memo |

| Variation #7 | tot odp/swp dr memo |

| Variation #8 | tot odp |

What to do if you see a tot odp swp cr memo charge

There is some good news is you see tot odp swp memo on your Chase statement – there is a little time to fix it and avoid up to $102 in overdraft fees.

Remember, the TOT stands for Temporary Overdraft Transaction, which means that Chase hasn’t yet reconciled your account for the day. Chase actually offers you a brief grace period to get your checking account balance back to positive (or at least less negative) to avoid fees. If you make a deposit via a branch, ATM or the Chase mobile app before 11:00pm EST on the same day that your account balance turned negative, Chase will apply those transactions to your daily balance. If your account balance turns positive or less than $50 negative, then you face any overdraft fees that day. Even if you don’t have funds available to cover the entire negative balance, making a small deposit may help you eliminate one or two of those pesky $34 overdraft fees.

Chase does offer a few additional tools to help you avoid overdraft fees.

One of the simplest to setup is Chase’s automatic alerts, which can be sent to you via email, text or app notification. You can set the conditions you’d like to be notified about, such as a low balance or a large bill payment that was just made. Knowing that you’re at risk of overdraft fees gives the opportunity to easily prevent them by limiting your spending on your Chase debit card or by moving around money from other sources.

You can also choose to turn off overdraft protection on your Chase account. This can be a good choice if you’re frustrated by frequent overdraft fees, but it also means that if a purchase would push your account into negative territory then it will be declined.

An alternative is to select Chase’s Debit Card Coverage, which can provide a nice cushion in case of emergencies. Debit Card Coverage lets you use your debit card for essential purchases only, such as at gas stations, grocery stores and restaurants. Charges at other merchants will be declined (with no fee) if you don’t have the funds in your account to pay for them. You may still incur $34 overdraft fees for this coverage if your negative balance exceeds $50 and make purchases over $5.

Best apps to help you avoid Chase Overdraft fees

If you’re constantly seeing a variation of tot odp/swp cr memo on your Chase bank statement, it may help to find alternate ways to top up your checking account and avoid overdraft fees. And if you’re finding yourself low on cash at the end of the month, you’re not alone. In fact, a shocking 7 out of 10 Americans live paycheck to paycheck. To avoid the stress that comes with financial uncertainty, a cash advance app can be the perfect solution.

For borrowing between $100 to $2,500 to cover bills, subscriptions, or emergency purchases, PockBox and Earnin offer alternatives to help you avoid overdrafts.

Use PockBox to Borrow up to $2,500 even if you have bad credit

PockBox is the perfect app to get cash advances of up to $2,500.

The process is sleek and straightforward so you can top up your checking account fast. You’ll simply need to give some information about yourself and the PockBox app will connect you to the best lender possible and approve you in a matter of minutes.

Quick, easy, and the fast way to get rid of a tot odp/swp cr memo on your next bank statement.

Borrow up to $2,500 without stressing over bad credit >>> Browse PockBox Now

Try Albert for cash advances up to $250 with no interest and no credit check

Albert makes it easy to access quick cash with no interest and no-fee cash advances up to $250. There’s no credit check to be eligible, and you don’t need to move your direct deposit if you don’t want. Although switching to an Albert account will put cash advances in your account almost instantly and let you access your paycheck up to 2 days early.

No-interest, No-fee cash advances for up to $250 >>> Create an Albert account in two minutes

Looking for more cash advance apps?

The new wave of alternate lending apps means you’re no longer stuck in your bank’s service offerings (and paying frustrating bank fees). As a Chase Bank customer, it helps to know your options.

We’ve rounded up the top cash advance apps to help you say goodbye to the frustration of a confusing charge. These are picked based on cost, ease of application, eligibility criteria, and safety. Click below to explore your options and make tot odp swp cr memo a thing of the past.

Check out the full list below.

FIND OUT MORE >>> 9 Best Cash Advance Apps of 2023

Can you get rid of a tot odp swp cr memo charge?

Yes.

If seeing a pending tot odp\swp cr memo charge on your account, or your account has been overdrawn, it helps to know how to get rid of this charge.

As this is an overdraft fee, you’ll need to get in touch with your bank and speak to a bank manager or customer service representative. Banks aren’t in the habit of wiping every overdraft fee. But you may be able to wipe one or two charges per year if you have a good credit history.

For more help removing an unwanted bank charge, check out our What is an Overdraft: Industry Guide (with bonus step-by-step walkthrough for reversing overdraft fees).

GET THE GUIDE >>> What is an Overdraft: Industry Guide [UPDATED]

Final thoughts and what to do next…

In the short term, you know what it means when you see tot odp swp/cr memo on your next bank statement. This charge relates to overdraft protection transfer fees. You have several options to ensure you’re in control of your money in the long term.

If transferring money from a linked savings account doesn’t appeal to you (and you’d like to say goodbye to overdraft fees for good), it may be worth looking into a cash advance alternative to keep your checking account topped up.

Apps like PockBox allow you to borrow up to $2,500 while cash advance apps like Albert can put $250 in your pocket fast. At a cheaper cost than overdraft fees and missed payment penalties, weighing up the advantage of cash advance apps can mean the confusion of a tot odp swp cr memo charge (and the fees that come with them) becomes a thing of the past.

BEFORE YOU GO…

Never get caught short of cash again with these quick and hassle-free options:

Watch: How to set up Chase Overdraft Protection

WAIT! Why borrow quick cash when you can earn it?!

Cash advance apps can be a great tool for getting a little extra cash when you need it, but you’ll need to repay it – plus fees – wihtin a week or two. Did you know there’s an easy way to earn extra cash that’s yours to keep?

KashKick is a wildly popular service that lets you earn money for playing games, completing surveys, signing up for trial offers and more. (You’ll even earn cash for just completing your profile!) You can earn cash today and withdraw your earnings through PayPal once you’ve reached $10. You can earn over $100/month with KashKick – and you don’t need to spend a dime or take out your credit card to do it.

There are dozens of high-paying offers available on KashKick, and if you’re into playing new games on your phone, you can earn some serious cash for doing what you love. Though offers change regularly, there are currently1 more than three dozen offers available where you can earn cash – sometimes over $100 – just by downloading and playing popular games like Coin Master, Monoply Go, Bingo Blitz, and more. These games are all free to download, and no in-app purchases are required to earn with KashKick.

Get paid to play on your phone >>> Check out KashKick

Mitchel holds a Bachelors of Business Administration in Finance from The Goizeta School of Business at Emory University and a Masters of Business Administration from The Haas School of Business at The University of California.

- Cleo App Review – $250 Cash Advances and Wiseass AI Money Management - April 24, 2024

- FloatMe Review – Simple $50 Cash Advances with Low Fees - April 17, 2024

- MoneyLion App Review: Save, Invest & Borrow up to $1,000 in One Simple App - April 15, 2024

- As of February 13, 2024. Offers may change and may not be available to all users. Eligibity requirements apply. See KashKick's Terms of Service for full details.

- Subject to eligibility. Amounts range from $20-$250, and $20-$100 for first time users. Amounts subject to change. Same day transfers subject to express fees.