Editor’s Note: Overdraft Apps provides detailed product reviews and recommendations based upon extensive research and our own hands-on testing. We may earn a referral fee when you sign up for or purchase products mentioned in this article.

Need cash but low on funds? Several banks let you withdraw money from the ATM even if you have insufficient funds. You’ll incur a fee for the convenience, but if you desperately need cash then a fee can be the least of your worries. Read on to discover how to overdraft at an ATM, protect yourself against overdraft fees, and compare no-fee alternates to ATM overdrafts.

Find Loans for $100 - $2,500 in Minutes

- Multiple lenders compete for your business

- No minimum credit score

- View loan offers in minutes - No application fees, no obligation

How to overdraft at an ATM: Step by step guide

Step One: Opt into your bank’s overdraft coverage or set up overdraft protection on your account. This allows you to withdraw money from an ATM even if you don’t have money in your account.

Step Two: Visit an ATM and request an amount that is larger than your available balance. Some ATMs will warn you that the transaction will cause you to incur an overdraft fee. If you choose to continue with the transaction, the ATM will dispense the cash you requested (final transaction approval will be at your bank’s discretion).

That’s it.

That’s every step.

You may also be subject to ATM fees, but these exist outside of any overdraft fees charged by your bank.

| 🤓 Overdraft Apps Tip: If you have insufficient funds, your bank will automatically decline an ATM withdrawal (with no fee charged) unless you’ve opted in and accepted potential overdraft fees. |

FIND OUT MORE >>> Can you overdraft a negative account? 🤔

Can you overdraft a cash advance app card at an ATM?

Apps like Dave, Current and Chime offer features like no-fee overdrafts, early access to your paycheck and no or low-fee cash advances to help you juggle your finances.

They also provide no-fee debit cards that you can use to make purchases or ATM withdrawals.

However, none of these services allows you to overdraft your debit card at an ATM.

You can’t overdraft Chime or a Current card at an ATM. If your balance is low or negative, Chime and Current can provide no-fee overdrafts for up to $200 of debit card purchases instead.

What is the daily overdraft amount limit on ATMs?

There are no set limits on how much you can overdraft at an ATM.

Overdraft amounts vary across financial institutions and many times are tailored to each individual account holder.

Other factors to consider are whether you are using your bank’s ATM or those owned by another financial institution. Sometimes, only your banks’ ATMs will let you overdraft.

As a general rule, new account holders and those with poor credit scores are often limited in the amount they are allowed to overdraft (usually around $100 to $300).

More established customers with higher credit scores may be allowed to overdraft in excess of $1,000.

Even if you ask your bank what their particular policy is, they won’t be able to quote you overdraft figures until you sit down with them and fill out the paperwork.

When you are at another bank’s ATM the rules for overdrawing will most likely be different and won’t be as high as your bank will allow. Some financial institutions won’t permit non-bank member overdrafts while others limit overdrafts to smaller amounts.

FIND OUT MORE >>> How much can I overdraft my checking account? 🤔

How much are overdraft fees on ATM withdrawals?

ATM overdraft fees vary from bank to bank.

ATM overdraft fees are typically about $35, though some banks have reduced or eliminated overdraft fees for small amounts – for example, Chase’s new overdraft policy offers no-fee overdrafts for up to $50, and no overdraft fees on transactions for less than $5.

Your bank’s overdraft fee is usually a flat rate, meaning that you’ll pay the same $35 whether you take out $20 or $100 from the ATM. Once your account is overdrawn, your bank will likely charge you an additional fee for every transaction you complete – many banks will charge you for up to five overdrafts in a single day, which can cost you $175 or more.

If you really need cash and have decided to pay the fee to overdraft at an ATM, you may be better off taking out more money than you think you need to limit fees, provided you have a clear path to quickly paying back.

You’ll generally need to agree to pay an overdraft fee before withdrawing cash from an ATM. For example, with Bank of America you’ll need to authorize the overdraft transaction at the ATM in order to get your cash. Note that if you are using an ATM from another bank or service provider, you may not be advised about the overdraft fee.

FIND OUT MORE >>> Check out our list of overdraft fees by bank 👈

What banks let you overdraft at an ATM?

| Bank | ATM Overdrafts |

| Academy Bank | ✔ |

| Bank of America | ✔ |

| BBV Compass | ✔ |

| BMO Harris Bank | ✔ |

| Capital One 360 | ✔ |

| Charles Schwab | ✔ |

| Chase | ✔ |

| Citibank | ✔ |

| Citizens Bank | ✔ |

| Fifth Third Bank | ✔ |

| HSBC Bank | ✔ |

| KeyBank | ✔ |

| M&T Bank | ✔ |

| PNC Bank | ✔ |

| Regions Bank | ✔ |

| Santander Bank | ✔ |

| TD Bank | ✔ |

| Truist Bank | ✔ |

| Union Bank | ✔ |

| USAA | ✔ |

| U.S Bank | ✔ |

| Wells Fargo | ✔ |

| Woodforest Bank | ✔ |

Will an ATM overdraft affect your credit score?

No. ATM overdrafts do not impact your credit score. It actually helps maintain it from having a black mark for having an insufficient fund item.

The only time an ATM overdraft becomes a problem is if you take too long to repay the overdraft amount.

DEALING WITH POOR CREDIT? Boost your credit score in as little as $5/month 🤑

What are my options if I don’t want to pay ATM overdraft fees?

Some banks have services to automatically transfer money from one account to another – such as checking accounts or savings accounts.

Once you overdraw your balance from one account (the one you used your debit card with), it will automatically take funds from your other account to cover the excess.

This typically incurs a linked account transfer fee. However, these are less than overdraft fees.

FIND OUT MORE >>> Can you overdraft a savings account? 👈

How to top-up your checking account instead of overdrafting

PockBox: Borrow up to $2,500 even if you have bad credit

Answer a few quick questions, and PockBox will instantly fetch loan quotes from up to 50 lenders, so you can find the offer that works best for you.

Loans start at $100, and you may be able to borrow up to $2,500. With most lenders, you can get your loan by the next business day, and sometimes even faster.

PockBox is free to use, and there’s no obligation. Many lenders on PockBox specialize in borrowers with bad credit, so even if you’ve been turned down elsewhere, you may still qualify for a loan.

Compare Your Loan Options (Up to $2,500)

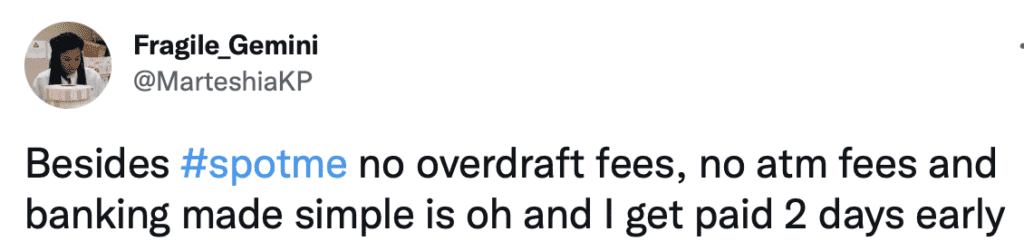

Chime: Overdraft up to $200 with ZERO overdraft fees

Chime’s SpotMe® feature lets you make debit card purchases or ATM withdrawals that overdraw your account with no overdraft fees. Limits start at $20 and can be increased up to $200.2

There is no cost to enroll in SpotMe, and once you set up your account to receive a qualifying direct deposit of $200 or more a month, Chime will cover up to $200 in overdrafts on your account.

Fee-free overdrafts up to $200 >>> Check out SpotMe 👈

What to do next…

ATM overdrafts provide extra cash when you need it, but you’ll need to stay on top of the high fees to avoid falling deeper into debt.

Wherever possible, use your own bank’s ATM so you won’t be refused an overdraft.

When you’re aware of the absorbent amount of fees that come with ATM overdrafts, it’s easier to assess whether the protection is worth having or if opting for an alternate service is the better option.

WAIT! Why borrow quick cash when you can earn it?!

Cash advance apps can be a great tool for getting a little extra cash when you need it, but you’ll need to repay it – plus fees – wihtin a week or two. Did you know there’s an easy way to earn extra cash that’s yours to keep?

KashKick is a wildly popular service that lets you earn money for playing games, completing surveys, signing up for trial offers and more. (You’ll even earn cash for just completing your profile!) You can earn cash today and withdraw your earnings through PayPal once you’ve reached $10. You can earn over $100/month with KashKick – and you don’t need to spend a dime or take out your credit card to do it.

There are dozens of high-paying offers available on KashKick, and if you’re into playing new games on your phone, you can earn some serious cash for doing what you love. Though offers change regularly, there are currently1 more than three dozen offers available where you can earn cash – sometimes over $100 – just by downloading and playing popular games like Coin Master, Monoply Go, Bingo Blitz, and more. These games are all free to download, and no in-app purchases are required to earn with KashKick.

Get paid to play on your phone >>> Check out KashKick

- As of February 13, 2024. Offers may change and may not be available to all users. Eligibity requirements apply. See KashKick's Terms of Service for full details.

- Banking services provided by The Bancorp Bank, N.A. or Stride Bank, N.A., Members FDIC. SpotMe® on Credit is an optional, no interest / no fee overdraft line of credit tied to the Secured Deposit Account available to qualifying members with an active Chime Credit Builder Account. SpotMe on Debit is an optional, no fee overdraft service attached to the Chime Checking Account available to qualifying members after Visa debit card activation. Both SpotMe on Credit and SpotMe on Debit are sometimes collectively referred to as “SpotMe” or, if you have signed up to use SpotMe with only one account, “SpotMe” means the elected service. To qualify for SpotMe, you must receive $200 or more in qualifying direct deposits to your Chime Checking Account each month.