Editor’s Note: Overdraft Apps provides detailed product reviews and recommendations based upon extensive research and our own hands-on testing. We may earn a referral fee when you sign up for or purchase products mentioned in this article.

30-SECOND SUMARRY: Short on funds for the footy? Keen to grab a parmy at the pub? Need a little extra to cover the price of petrol? Whether you’re in need of quick cash for something small or you’re facing more serious cash shortfalls like covering your rent, having the ability to extend your bank balance beyond zero can be a lifesaver. Here’s what you need to know about overdrafts with CommBank, NAB, Westpac and ANZ.

Overdrafts are like a brief loan arrangement.

You can spend more than you have and pay back your bank later on. Sounds good, right?

Here’s the catch…

Following the Banking Royal Commission and changes to the Banking Code of Practice 2019, overdraft facilities are no longer offered by most of the Big Banks, including:

- Commonwealth Bank

- NAB

- Westpac

- ANZ

With banks no longer able to charge dishonour fees or offer informal overdrafts on basic accounts, you may need to look for alternative ways to top up your savings account. To help you understand the Aussie overdraft landscape, read on for a full breakdown of previous overdraft policies, fees and protection available.

What banks allow overdrafts in Australia?

Not many. The Banking Royal Commission found many low-income bank customers were’t made aware of their options for basic, no or low-fee banking products.

As an example, ANZ sent out 300,000 letters to customers offering them overdraft facilities without actually checking if they could afford the extra debt,

With this just one of many horror stories, the ACCC granted interim authorisation to allow the Australian Banking Association (ABA) to take immediate steps to make certain changes to the Banking Code of Practice.

This meant banks agreed to not charge dishonour fees, overdrawn fees or allow informal overdrafts on basic bank accounts.

In short, most banks – including the ‘Big Four’ Banks – have mostly removed personal overdrafts as a product offering.

Who are the ‘Big Four Banks’?

The ‘Big Four Banks’ refers to the four largest and most influential banking institutions in Australia.

Here’s a quick refresh in case you’ve been living under a rock:

- Commonwealth Bank of Australia (CBA): Founded in 1911, the Commonwealth Bank is the largest bank in Australia and offers a wide range of financial products and services, including personal and business banking, wealth management, and insurance.

- Westpac Banking Corporation: Established in 1817, Westpac is one of Australia’s oldest and most distinguished banks. It provides a comprehensive suite of financial solutions, including retail, business, and institutional banking, as well as wealth management and insurance.

- Australia and New Zealand Banking Group (ANZ): Founded in 1835, ANZ operates in more than 30 countries worldwide. ANZ offers a broad range of banking and financial services, including retail and commercial banking, wealth management, and corporate banking.

- National Australia Bank (NAB): With a history dating back to 1834, NAB is known for its diverse range of financial services, including personal and business banking, wealth management, and investment solutions.

Since these banks dominate the Australian banking industry, chances are you’ve either got an account with one of them, or you know someone who does.

Read on for a breakdown of which Australian banks offer overdrafts, how much you can overdraw your account, and what you should expect to pay.

Commonwealth Bank: Overdraft Limits, Fees & Protection [Available]

No matter how closely you manage your finances, life happens, and you can quickly end up with a shortage of funds.

Whether it’s for something big (like your car rego), or something smaller (like paying back a mate for their shout at the pub), you may be able to access a personal overdraft using the Commonwealth Bank’s Overdraw feature.

How does a Comm Bank overdraft work?

Your overdraft facility is connected to your CommBank Everyday account, so you can easily access extra funds ranging from $100 to $20,000 (where eligible).

Once you’ve overdrawn your account, any money you put into your transaction account is automatically used to repay your overdraft balance – such as your salary, transfers and other deposits.

You aren’t obliged to make set minimum monthly repayments on the money you borrow – but you will be charged interest until you return a positive balance. So, while there’s no set minimum required, Comm Bank recommends repaying your overdraft ASAP to minimise any interest or fees.

CommBank may allow overdrawing on transaction accounts (like Smart Access, Complete Access, and Everyday Offset) for the following types of payments:

- Direct Debits (e.g. gym memberships, bills, and loan repayments)

- PayTo payments

- Cheques

- Scheduled BPAY payments

- Transactions conducted using your linked CommBank card

How much does a Comm Bank overdraft cost?

Commbank’s Overdraw is free to set up and won’t cost you anything if you don’t use it. If you choose to use your overdraft, you’ll pay interest on the money you borrow (the CommBank overdraft interest rate is 14.90% p.a and charged monthly) plus a possible fee.

For example… if your overdraft limit is $1,000, but you only need a $50 overdraft, you’ll only be subject to interest charges on the $50 you use (plus your monthly fee).

According to the Commonwealth Bank, if the balance isn’t restored to a positive by midnight of that day (Sydney/Melbourne time), you will incur a $15 overdraw fee. This fee is generally applied on the subsequent business day. 1

In some circumstances, you may be able to avoid a fee. If the highest amount used from your overdraft the month before is $15 or more, you’ll be charged $15 for that month. If it’s less than $15, you won’t be charged a fee.

Bonus: Wondering how to check your Commonwealth Bank overdraft limit?

If you’re a CommBank customer, log onto your NetBank account or use the CommBank app to view your current personal overdraft limit. Limits start at $100, and you can apply to increase your overdraft limit if you’re in need of more flexibility on your transactions.

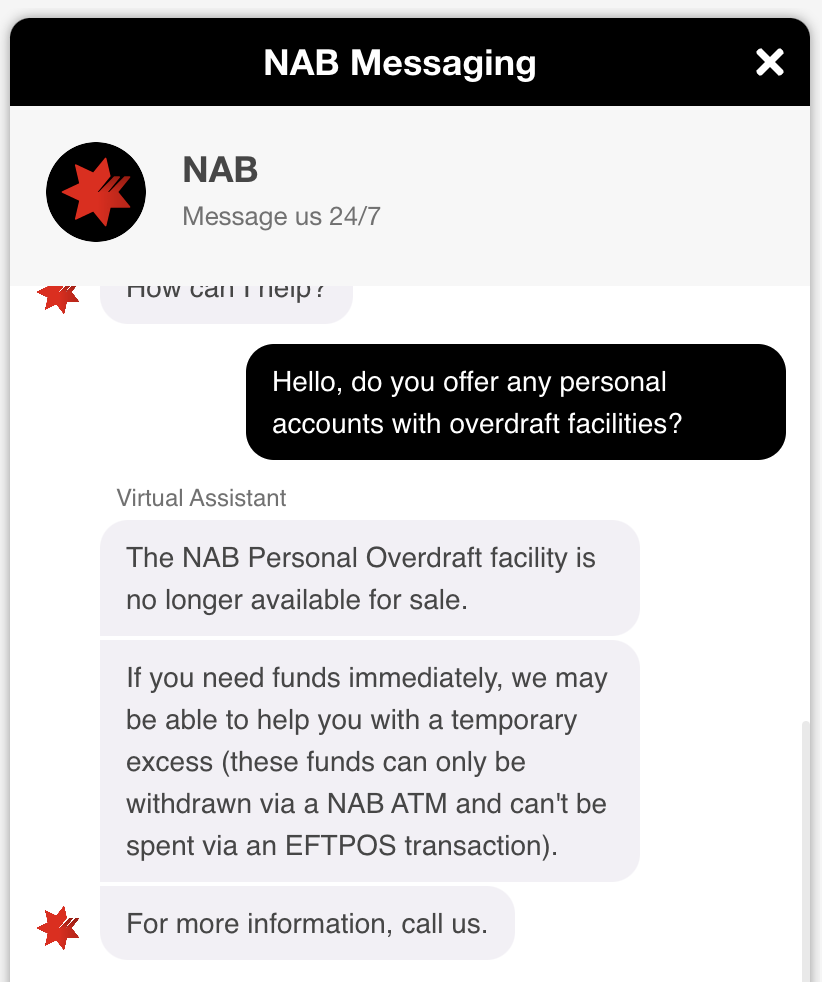

NAB: Overdraft Limits, Fees & Protection [No Longer available]

NAB’s Personal Overdraft allows you to access extra cash when you need it with your NAB transaction account (up to an approved limit).

At least… it did.

As of 2023, this product is no longer available. We asked NAB’s helpful chatbot for more information and got the definitive answer below.

We’ve still rounded up NAB’s previous overdraft policy. If you’re a current NAB customer with a Personal Overdraft Facility, you can continue to use this product as usual. If you’re looking for emergency cash, you may be better off weighing up other options with popular payday advance apps including InstaPay, BeforePay and MyPayNow.

So, can you still overdraw your NAB account?

The answer is yes – but not on purpose. Here’s what NAB has to say about transactions that inadvertently overdraw your account:

“If you try to make a transaction that’ll overdraw your account (or exceed your agreed overdraft limit), we may honour or decline the transaction. We’ve abolished fees for overdrawn accounts, but if we let the transaction go through, you might be charged interest (at our default rate) on the overdrawn amount for the period of time your account remains overdrawn.”

Any sort of debit can overdraw your NAB account, including withdrawals, debit card purchases and even any fees the bank charges you. If you do go beyond your bank balance, you’ll have seven days to return the overdrawn amount to your account before default interest is charged.

How did an NAB overdraft work?

NAB’s Personal Overdraft was previously linked to an NAB Classic Banking account or NAB Retirement Account. If approved, you could withdraw money up to an approved amount so you can go in and out of a negative balance with your transaction account.

Interest on your NAB overdraft would only be calculated when your end-of-day account balance was negative. This meant you could go in and out of negative balance during the day, and as long as your end-of-day account balance was positive, you wouldn’t be charged any interest.

If your end-of-day balance was negative, NAB’s variable interest rate would apply (12.77% p.a. at the time of writing).

You’d also be charged NAB’s Overdraft Line Fee – a fee charged every six months (March and September) for the convenience of having overdraft facilities. Although the minimum fee was $35, this amount may increase based on your approved limit.

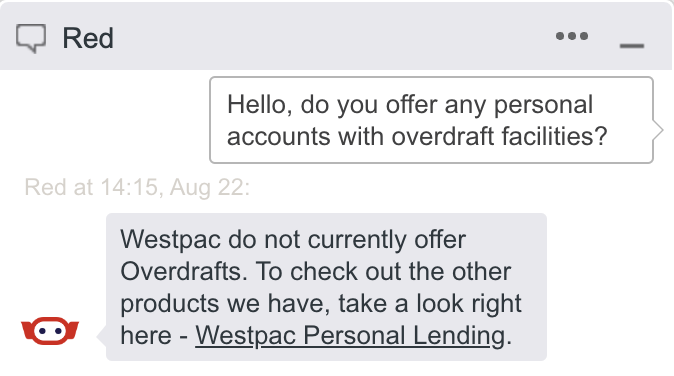

Westpac: Overdraft Limits, Fees & Protection [No Longer available]

Westpac’s Personal Overdraft is connected to your everyday Westpac Choice bank account. This allows you to overdraw your available balance (up to an agreed limit from $250 to $25,000) to cover life’s unexpected costs and emergencies.

But, just like NAB’s overdraft, this product is no longer available.

As of 2023, Westpac is no longer offering overdraft facilities to new customers. Westpac’s handy chatbot Red confirmed the bad news below.

Current customers with overdrafting facilities may still access this product. We’ve still put together everything you need to know about Westpac’s previous overdraft policy, but if you’re short on cash and looking for other options, Australia’s growing market of instant loan apps can help you tap into $100 or more of your wages before payday when you’re short of cash.

How did a Westpac overdraft work?

A Westpac overdraft allows you to access your personal overdraft funds through your Westpac Choice bank account using:

- Online, Mobile, Telephone and Tablet Banking

- EFTPOS

- Debit Mastercard

- Cheque

- BPAY®

- In branch

With overdraft limits running from $250 to $25,000, you’d only pay interest on the funds you needed, which offered a handy (and affordable) safety net when your funds were low.

Westpac’s variable interest rate applied on all overdrafts (12.09% p.a. at the time of writing ). Overdraft facilities came with a $0 lending establishment fee and just a $6 monthly loan account fee.

Like NAB, interest on your Westpac overdraft would only be calculated when your end-of-day account balance was negative (or to a balance within the agreed overdraft limit). If your end-of-day account balance was negative, you would be charged a $15 fee for each day until your account was returned to a positive balance.

ANZ: Overdraft Limits, Fees & Protection [No Longer available]

ANZ previously had two options for overdrawing your account.

- ANZ Assured: A credit limit of either $500 or $1,000 to temporarily cover unexpected cash shortfalls (20.10% p.a.)

- Personal Overdraft: A credit of $1,000 or more (up to an approved limit) to be used whenever you need it (15.95% p.a.)2

Both overdraft facilities gave ANZ customers access to extra cash when they needed it. But, like Westpac and NAB’s similar overdraft products, this has gone the way of the dinosaurs.

If you’re a current ANZ customer with a Personal Overdraft Facility, your use will be unaffected. Although this product is no longer available, we’ve still rounded up ANZ’s previous overdraft policy and you may still be eligible for an overdraft by contacting your local ANZ branch.

How did an ANZ overdraft work?

ANZ’s Personal Overdraft was a credit facility connected to selected ANZ everyday accounts. These included:

- ANZ Access Advantage

- ANZ One

- ANZ Premium Cash Management

With a $1,000 minimum limit, this feature gives you the peace of mind of being able to pay anything – from last-minute bills to emergency expenses – and pay back the overdrawn amount on your next deposit.

When you need to make a purchase, simply access funds in the way you normally would (including the ANZ App, ANZ ATMs, EFTPOS and Internet Banking, or at any ANZ Branch).

ANZ’s variable interest rate applied on all overdrafts (15.95% p.a.) with an initial approval fee and credit facility fee on top. Approval fees ranged from $100 (for a credit limit under $20,000) to $500 (for a credit limit of $50,000 and over). Credit facilities ranged from $200 a year (for a credit limit under $20,000) to 1.7% of the limit per year (for a credit limit of $20,000 and over).

Australian Bank Overdrafts: The Final Word

Following changes to the Banking Code of Practice, overdraft facilities that force you into a negative balance (with interest paid on that balance) are no longer offered by most banks. Today, strict eligibility is required for overdraft products.

With limits on how many of the ‘Big Four Banks’ offer personal overdrafts, not all bank customers will have the option. As with any financial choice you make, compare your options to get the best deal possible.

Whether that means applying to your bank’s overdraft facility or accessing part of your wages early with a $100 loan from a pay advance app like BeforePay or InstaPay, the more you understand your options, the more control you’ll have over your finances and future.

Check out our most popular resources before you go: