Editor’s Note: Overdraft Apps provides detailed product reviews and recommendations based upon extensive research and our own hands-on testing. We may earn a referral fee when you sign up for or purchase products mentioned in this article.

Usually, a prepaid card means high fees and few benefits. KOHO aims to shake up that model with a full-featured plan you can qualify for with no monthly fees, and generous cash-back offers that can actually put money back in your pocket.

Plus, with KOHO Cover, you can get up to $50 in instant overdraft protection (and increase your limit to up to $250) with no interest to pay bills or make purchases.

But not everything is perfect. Before you jump in to get your cash advances, you should fully understand what you’ll need to qualify, and how much the advances will cost you.

Luckily, we’ve got you covered with all you need to know in our KOHO review.

Access up to $250 in overdraft protection >>> Check out KOHO

What is KOHO?

KOHO is a mobile banking app that’s helping over 1 million Canadians budget, spend, and save smartly. The app offers three paid tiers of full-service mobile banking.

The KOHO app can give you powerful banking features right from your phone, including:

KOHO debit card: KOHO’s prepaid Mastercard® is the card that can actually pay you for a change. You can earn up to 2% cash back on groceries, dining and transportation, plus up to 0.5% on everything else. Unlike other prepaid cards, your deposit earns interest, too – currently a healthy 5%! Plus, there’s no credit check to qualify.

Cover Cash Advance: This grants overdraft protection of up to $250 with no interest or late fees. While you can’t withdraw the amount in cash, you can use it to pay bills or spend it almost anywhere via your KOKO debit card.

Credit Builder Accounts: KOHO offers two lines of credit with no credit check or interest. One requires you to provide a cash deposit as collateral, while the other is unsecured, but approval is guaranteed for both. KOHO reports them to Equifax.

High-Interest Savings Account: KOHO lets you earn up to 5% interest on the cash you deposit in your account, depending on your subscription plan. In addition, the first $100K is eligible for CDIC protection.

Get up to 2% cash back on groceries, dining, and more >>> Check out KOHO

KOHO Cash advances: Everything you need to know

KOHO’s cash advances, referred to as “Cover” let you get $50 for starters. Your limit can increase to up to $250 as you build up a track record of timely repayments.

There is no interest or credit check to use KOHO Cover, and no late fees, express fees, or tips. Best of all, the funds reach you instantly, unlike most apps, where the money will take multiple business days to get to you unless you pay an express fee.

Instead of the usual model that charges you turbo fees to get your money in minutes, KOHO requires you to sign up for their Cover program, which is charged separately from the app’s paid subscriptions.

While KOHO claims that everyone qualifies for their cash advances, the Cover service is not available on brand-new accounts, and you have to jump through a few hoops to gain access, including showing consistent activity in your KOHO account.

If you don’t qualify at first, you can increase your chances of becoming eligible by:

- Adding funds to your KOHO account

- Keeping a balance and spending with KOHO

- Setting up a direct deposit to your KOHO account

- Using other KOHO services like credit building

Once you’re eligible, KOHO will invite you to subscribe to Cover. If you accept, it’ll add up to $50 of reserve cash to your account. If you ever exhaust your ordinary funds, the Cover money will go toward any purchases that would otherwise cause an overdraft.

As long as your subscription stays active, you won’t have any minimum payments. However, paying your balance off in a timely manner can increase your Cover credit limit by up to $250.

Start earning cash back with a 30 day free trial >>> Check out KOHO

How Do KOHO Cash Advances Work?

With KOHO, you can start with up to $50 in overdraft protection, and your limit can increase to up to $250 as you build up a track record of timely repayments. You can see your KOHO overdraft limit right in the app, so you know how much you have available, and KOHO will automatically transfer funds to cover purchases or bill payments that could push your balance into negative territory.

There is no interest or credit check to use KOHO Cover, and no interest, late fees, express fees, or tips. You do need to pay a $5/month fee to have access overdrafts.

Cover is not available on brand new accounts, and you have to jump through a surprising number of hoops to gain access.

To get started, visit the KOHO website or download the mobile app from the App Store or Google Play. From there, you can register for an account using your email and password. Next, KOHO will ask you some basic details about yourself, including your:

- Name, birthday, and address

- Occupation

- Mobile number

Once you confirm a code KOHO texts to your phone, it’ll attempt to verify your identity. KOHO may be able to complete the process automatically by matching your name, address, and date of birth to your credit file.

If it can’t, you’ll need to provide a picture of a government-issued photo ID. Some valid options include a:

- Canadian or foreign passport

- Permanent Resident card

- Driver’s license or provincial photo ID card

Once that’s done, KOHO will activate your account. It should put you on the Easy plan by default, which is KOHO’s free subscription tier. In addition, it’ll tell you whether you’re eligible for the Cover feature.

KOHO isn’t very transparent about what it takes for users to qualify for Cover, but you must at least have an active membership and not have failed to pay anything you owe them. KOHO also states that no credit checks are involved.

If you don’t qualify at first, you can increase your chances of becoming eligible by:

- Adding funds to your KOHO account

- Keeping a balance and spending with KOHO

- Setting up a direct deposit to your KOHO account

- Using other KOHO services like credit building

Once you’re eligible, KOHO will invite you to subscribe to Cover. If you accept, it’ll add up to $50 of reserve cash to your account. If you ever exhaust your ordinary funds, the Cover money will go toward any purchases that would otherwise cause an overdraft.

As long as your subscription stays active, you won’t have any minimum payments. However, paying your balance off in a timely manner can increase your Cover credit limit up to $250.

Get up to $250 with no interest or credit check >>> Check out KOHO

How Much Does a KOHO Cash Advance Cost?

KOHO cash advances don’t involve any one-time fees, and there’s no interest on your outstanding balances. KOHO won’t ask you for tips either, and since the funds show up in your account as soon as you subscribe to Cover, there’s no need for an express fee, like many other cash advance apps charge.

However, that doesn’t mean the KOHO cash advance is free.

To maintain access to the feature, you must pay for the Cover subscription, which starts at $2 per month and goes up if you decide to unlock higher limits for your cash advance amounts. This is on top of the base KOHO Essentials subscription, which costs $4 per month (though you can get this fee waived by making regular deposits to your account).

Your initial credit limit can only be $50 at most and $20 at the minimum. Although this sounds somewhat expensive, it can be a very reasonable cost considering the perks, especially if you make multiple advances each month.

The catch is that you may not be eligible for Cover unless you use some of KOHO’s other features, like its credit-building products. Unfortunately, those come with their own monthly subscription fees.

If you want to get a cash advance from KOHO, you’ll be paying at least $6/month in subscriptions, which can be steep considering the $50 limit, so you should be careful if you’re not planning to use the app’s services on the regular.

Get up to $250 with no interest or credit check >>> Check out KOHO

KOHO’s paid plans and their features

KOHO offers four different levels of membership, including a free plan that will meet many users’ needs. With KOHO, you can earn solid rates of cash back on all purchases (rare for a debit card!) as well as a decent interest rate on your balances.KOHO is one of the few financial apps that lives up to its claim of simple pricing and no hidden fees. A summary of the plan options:ESSENTIAL — $4/month or $48/year From April 20th, 2024, the essential plan includes 1% cashback on dining, groceries, and transportation you pay for with your KOHO debit card. You’ll also get up to 50% cashback on the vendors within KOHO’s network.Want to avoid the monthly fee? You can get the Essential plan with no fee if you set up a Direct Deposit with KOHO or deposit $500 or more each month on your KOHO account. With the ability to get the monthly fee waived and generous cashback offers on some debit card purchases, KOHO can actually pay you!EXTRA — $9/monthYour monthly fee bumps up to $9 with Extra, but your cashback tiers all double to 2% on groceries, dining, and transportation, plus 0.5% on everything else.These cash-back rates are better than what many credit cards offer and, if you spend over $125 KOHO on groceries, restaurants, and getting around town each week, you’ll earn back an even higher percentage.KOHO strongly hints that this plan will help you get access to overdrafts via KOHO Cover.EVERYTHING — $19/monthThe monthly fee leaps to $19 for this plan, and while you get real-time e-transfers and a few other small features, it’s probably not worth it for most folks.You’ll get a 30-day free trial to whichever plan you choose when you sign up with KOHO, so you can take the opportunity to see how much you’re earning via cash back and interest. You can change your subscription at any time in the app.Start earning cashback with a 30-day free trial >>> Check out KOHO

Is KOHO Legit?

Regardless of whether or not KOHO’s cash advance feature is a good deal, the company follows the standard regulations and guidelines that these types of financial apps are required to.

Founded in 2014, KOHO has a nearly decade-long track record and receives many positive reviews.

It currently has a rating of 4.6 out of 5 stars on Google Play, based on 66K ratings. Its score on the App Store is even more impressive, where it holds a solid 4.8 out of 5 stars based on 78.1K ratings.

KOHO has also received significant support from investors, raising $264 million over the last nine years. Its latest funding round closed in early 2022, in which it received a whopping $165 million from companies like:

- Eldridge

- Drive Capital

- Business Development Bank of Canada

The additional funds have allegedly put KOHO close to a whopping $1 billion valuation. However, as exceptional as those accomplishments are, not all of KOHO’s customers are satisfied with the company’s performance.

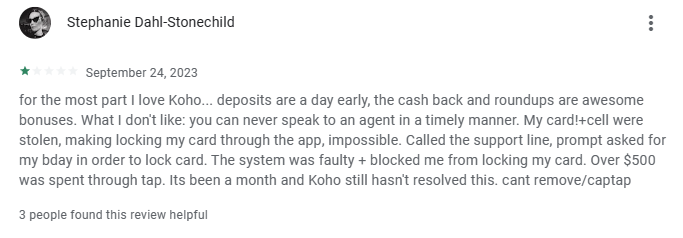

There are some consistent complaints in online reviews. One of the most significant is that KOHO continually updates its mobile app, and the changes often cause more problems than they solve.

For example, random technical glitches seem to be especially common. Users will suddenly find that they can’t log in to their accounts, their screens seem to load indefinitely, or their interface is unusable.

Perhaps even more importantly, some updates change the way features work for the worse, making them less useful to customers or even removing them altogether.

In other cases, the features stick around, but KOHO moves them to a higher-tier subscription account. That forces you to shell out a few extra bucks every month if you care about accessing them.

In addition, it’s often difficult to get in touch with customer support when you need them. Some customers experiencing highly time-sensitive issues have been unable to get an agent on the phone for assistance.

While there are some great features, you can see that some customers do leave pretty negative KOHO reviews. No product is without flaws. Be aware of these issues before committing to paid subscriptions.

Start earning cash back >>> Check out KOHO

Is KOHO worth it?

Most money apps will charge a relatively small subscription plus an express delivery to get the money in minutes. KOHO charges a paid plan for its general services, as well as a separate subscription for its Cover program to get cash advances, totaling $6/month at the very least and $21/month at most.

While the entry price may sound somewhat steep for small advances, the app offers other perks that can make it more than worth it. KOHO’s cashback offers are one of its biggest strengths and can put real money in your pocket. KOHO boasts that it has paid out over $15 million to its users!

If all you’re looking for is a quick cash advance app like KOHO, there might be other options better suited for you, such as Nyble, with its $150 advances for $8.99/month, and Bree with $250 advances for $2.99/month plus express fees.

Start earning cashback with a 30-day free trial >>> Check out KOHO

WAIT! Why borrow quick cash when you can earn it?!

Cash advance apps can be a great tool for getting a little extra cash when you need it, but you’ll need to repay it – plus fees – wihtin a week or two. Did you know there’s an easy way to earn extra cash that’s yours to keep?

KashKick is a wildly popular service that lets you earn money for playing games, completing surveys, signing up for trial offers and more. (You’ll even earn cash for just completing your profile!) You can earn cash today and withdraw your earnings through PayPal once you’ve reached $10. You can earn over $100/month with KashKick – and you don’t need to spend a dime or take out your credit card to do it.

There are dozens of high-paying offers available on KashKick, and if you’re into playing new games on your phone, you can earn some serious cash for doing what you love. Though offers change regularly, there are currently1 more than three dozen offers available where you can earn cash – sometimes over $100 – just by downloading and playing popular games like Coin Master, Monoply Go, Bingo Blitz, and more. These games are all free to download, and no in-app purchases are required to earn with KashKick.

Get paid to play on your phone >>> Check out KashKick

- Super Cash Advance Review: Convenient Add-on to Cashback Features - January 30, 2024

- KOHO Review: Up to $250 in Overdrafts and Generous Cash Back Offers - January 20, 2024

- OttoPay Review – Personalized Advice to Help You Pay Off Your Debt - November 29, 2023

- As of February 13, 2024. Offers may change and may not be available to all users. Eligibity requirements apply. See KashKick's Terms of Service for full details.