Editor’s Note: Overdraft Apps provides detailed product reviews and recommendations based upon extensive research and our own hands-on testing. We may earn a referral fee when you sign up for or purchase products mentioned in this article.

Overdraft fees could fall from $35 to as low as $3 under a proposed rule announced by the White House. The proposed changes would potentially eliminate billions of dollars in revenue for the nation’s biggest banks. Read on to learn how this change could affect millions of Americans living paycheck to paycheck.

Are you one of the millions of Americans who overdraft their bank account each year and face sky-high overdraft fees?

Relief may be on the way.

Americans paid nearly $300 billion in overdraft fees over the past two decades. Last year alone saw $9 billion drained from the bank accounts of hard working Americans.

Under a proposal announced by the White House, the Biden administration is looking to combat unnecessary financial pressure on Americans by dropping overdraft fees (typically $35) to as low as $3.

Here’s everything you need to know about the proposed changes that have the potential to eliminate billions in fee revenue for the nation’s biggest banks..

What are the proposed changes to overdraft fees?

The Consumer Financial Protection Bureau (CFPB) has unveiled a proposal to limit overdraft fees to as little as $3 per transaction.

This proposed change is approved by President Joe Biden who said in a statement, “This is about the companies that rip off hard-working Americans simply because they can”.

Bank overdrafts disproportionately affect low-income Americans who are at most risk of racking up large debts.

Under new proposals, relevant banks would be subject to tougher regulations on their overdraft programs – similar to credit cards – unless they agreed to lower customer fees.

“When companies sneak hidden junk fees into families’ bills, it can take hundreds of dollars a month out of their pockets and make it harder to make ends meet,” President Biden said in a statement. “This is about the companies that rip off hard working Americans simply because they can.”

“For too long, some banks have charged exorbitant overdraft fees — sometimes $30 or more — that often hit the most vulnerable Americans the hardest, all while banks pad their bottom lines,” President Joe Biden continued. “Banks call it a service — I call it exploitation.”

How the rule would lower your overdraft fees

Under the proposed rule, banks that let you overdraft would have two options if a customer overdraws their account.

Firstly, banks could charge consumers its actual cost to break even on providing overdraft services. This would require banks to show the CFPB the costs of their overdraft services – which banks may be hesitant to do.

The second option would mean adopting a benchmark fee. Recommendations for the proposed benchmarks range from $14 to as little as $3. These new rules would apply to banks and credit unions with more than $10 billion in assets – or about 175 of the nation’s biggest financial institutions.

If approved, these institutions could continue charging customers the actual cost to cover an overdraft, but they could no longer generate big bucks off the service.

Outside of overdrafts, banks could also provide small lines of credit to allow customers to overdraw their accounts as long as they comply with existing lending law, including the disclosure of any relevant interest rates.

Mitchel Harad, the publisher of Overdraft Apps, is cautiously optimistic about the proposed changes. “These changes could save millions of consumers who regularly overdraft several hundred dollars per year. However, it’s important to note that they have not yet been adopted so make sure you understand your bank’s overdraft policy and fees. More and more banks have eliminated or reduced overdraft fees, so it can pay to shop around!”

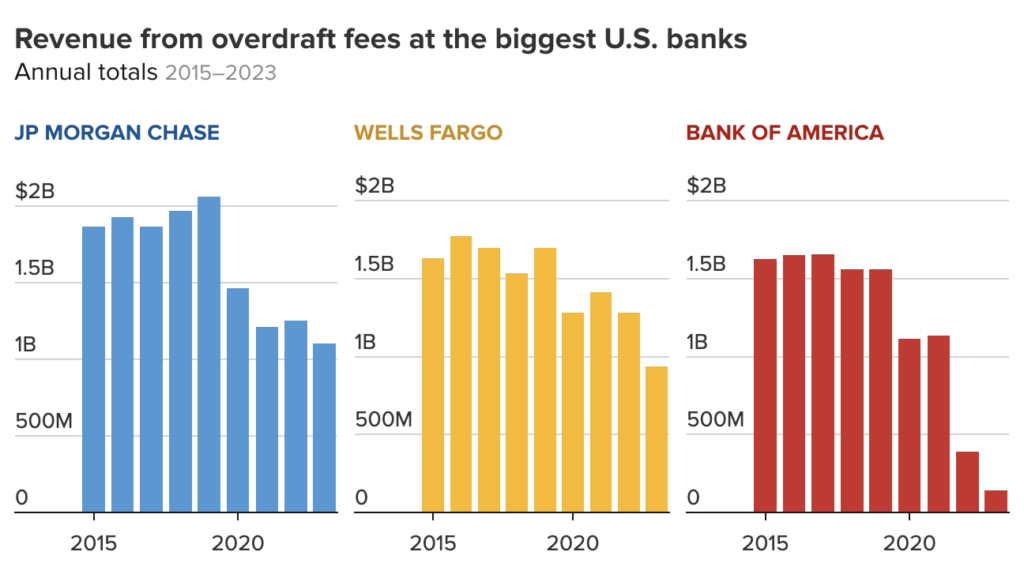

Overdraft fees have been BIG business for banks

Banks launched overdraft services for account holders in the 1990s. Created as a courtesy to customers at a time when paper checks could take days to clear, overdrafts have grown exponentially thanks to the growing popularity of debit cards.

Instead of letting checking holders take their balance below zero and avoid the embarrassment of a bounced check, millions of Americans now overdraft on ‘tap and go’ debit card transactions.

Today, overdraft fees have become a significant profit center as more and more customers overdraw their bank accounts – delivering billions in fees to banks.

Figures suggest 8% of bank customers – mostly low income – account for almost 75% of the revenue banks earn from overdraft fees.

According to research conducted by Bankrate, the average overdraft fee was $26.61. Some banks charge as much as $39.

While overdraft fees have fallen, an estimated 91% of checking accounts can still charge overdraft fees.

Banks are expected to fight the proposed restrictions and whatever rule is adopted is likely to be challenged in court.

| 💡Did You Know? Overdraft fees have become so popular (and profitable) that one bank CEO named his boat the ‘Overdraft’. |

What to do next

Most of the biggest banks have caved to recent pressure and added protection against potential overdraft fees.

U.S. Bank and Huntington Bank are two examples that offer customers a 24-hour grace period to cover the overdraft and avoid fees.

Bank of America has cut its overdraft fee from $35 to $10 two years ago and says revenue from overdraft fees is now less than 10% of what it had been.

The banking industry has been preparing for the proposal for months and is expected to fight the new regulations vigorously. The regulations could reach the Supreme Court before a final decision is made.

If adopted, the new regulations would go into effect in the autumn of 2025.

In the meantime, use our most popular resources to stay in control of your finances:

- Cash Advance Apps with No Direct Deposit Required

- Do These Things to Borrow $100 From Your Phone

- How to Pay for Gas on an Empty Bank Balance (Life Hack)