Editor’s Note: Overdraft Apps provides detailed product reviews and recommendations based upon extensive research and our own hands-on testing. We may earn a referral fee when you sign up for or purchase products mentioned in this article.

- Borrow $200 From Cash App: How to Get Two Hundred Bucks With No Credit Check - July 21, 2026

- How to Borrow $50 Instantly (2026): Best Cash Advance Apps - March 31, 2026

- Borrow $50 Instantly in Canada (2026): Best Cash Advance Apps - August 5, 2025

The main difference between Credit Strong and Self is the length of each credit builder loan, the cost of repayments, and the extra features included. Credit Strong reports a maximum $25,000 installment account compared to Self’s maximum of $3,600.

What is Credit Strong?

Credit Strong offers credit builder loans that may help you build your credit score through a positive payment history. With multiple credit-building loans to choose from, Credit Strong’s lowest-priced plan is pretty affordable and will set you back just $15 per month.

| Overdraft Apps Tip: The average Credit Strong customer sees their FICO Score 8 increase by more than 25 points within 3 months and 40 points after 9 months of opening their account. Credit Strong customers who make 12 on-time monthly payments more than double that score increase to almost 70 points. |

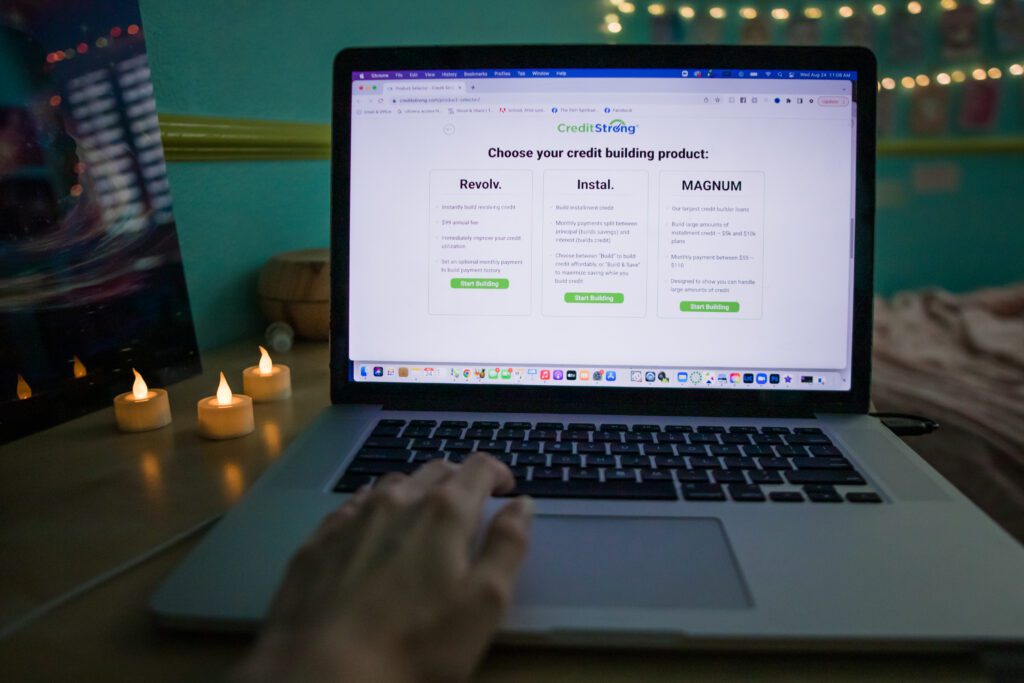

Credit Strong offers three products to help improve your credit:

- Revolv: The fastest way to improve your credit score is to lower your credit utilization (your account balance divided by your credit limit). Revolv helps lower your credit utilization and ‘instantly’ build revolving credit with no monthly payment required. The credit limit reported starts at $1,000 and maxes out at $3,000.

- Instal: Instal credit builder accounts report $1,000 or more of installment credit to the 3 major credit bureaus and build your savings while you build credit. Low, fixed monthly payments can be made over 24, 36, or 48 months and you can cancel at any time.

- CS Max: CS Max accounts are built for those who have cash but need credit. Up to $25,000 of installment credit is reported to the 3 major credit bureaus. With higher fixed monthly repayments, CS Max maximizes your total amount of credit and is not designed to build savings.

Learn More >>> Get started with Credit Strong 👈

| Product Name | CreditStrong |

| Loan Amounts | $1,000 to $25,000 |

| APR | 5.85% to 14.89% |

| Terms | 24 months to 10 years |

What is Self?

Self offers credit builder Plans designed to help bump up your credit score by reporting your on-time payments to major credit bureaus.

You can apply for a Self-loan online or via the Self Financial app even if you’ve currently got a low credit score (or no credit file at all).

When you open a Self Credit Builder Loan, you can choose between a monthly payment of 12 or 24 months. At the end of your plan, the payments you’ve made are yours (minus fees and interest) so you’re building savings and potentially boosting your credit score.1

Self reports your monthly payments to the three major credit bureaus (Equifax, Experian and Transunion). Automated monthly payments are available, so you never need to worry about missing a due date.

Build your credit and your savings >>> Check out Self 👈

| Product Name | Self |

| Loan Amounts | $600 to $3,600 |

| APR | 15.51% to 15.97% |

| Terms | 24 Months |

What Makes Credit Strong and Self Similar?

Both products potentially build your credit score by taking out a loan in your name, so you can make monthly repayments that are reported to the major credit bureaus.

Your payment history is the most influential factor in calculating your credit score. Both Credit Strong and Self target this factor by showing you can make on-time repayments.

Keep in mind, that you don’t get any money upfront with either product. When you sign up, Credit Strong and Self put your loan into a locked savings account as collateral.

You make principal and interest payments over the life of the loan. Once you reach the end of the payment schedule, your savings account is unlocked and you can access your funds.

Potentially, your on-time repayments will help increase your credit score. Either way, you walk away with a nice chunk of savings.

Here are a few more ways the two credit-building options compare:

- Both products allow you to build credit while saving money.

- Neither product requires credit checks or upfront security deposits.

- There’s no minimum income requirement to get started.

- Both products report to the three primary credit bureaus.

- Cancel your service at any time and receive a refund (minus interest and fees).

Credit Strong vs. Self: What are the Differences?

Credit Strong and Self both offer credit builder loans designed to help you improve your credit score and both products are designed to help potentially improve your credit score.

The key difference between Credit Strong and Self is:

- The length of the loan term

- The total monthly repayments

- The extra features included

Credit Strong has options that report up to $25,000 in installment credit compared to the $3,600 maximum offered by Self. Credit Strong’s larger amounts and longer repayment schedules might suit you depending on your current credit score and needs.

Credit Strong’s minimum monthly payment of $15 is lower than Self’s minimum monthly payment of $25.

Self also offers a secured credit card that can help build your credit and gives you flexible buying power anywhere that VISA is accepted. This only requires you to set aside a minimum of $100 from your credit builder loan as a security deposit (even if you haven’t fully paid off your loan).

Since a major factor in your credit score is your mix of accounts, with Self you get an installment loan and a credit card in one model which may help move the needle on your credit score.

Pros and Cons Compared

| Self Pros | Self Cons |

|---|---|

| Smaller loans available | Card does not offer rewards |

| Reports to the major credit bureaus | No money upfront |

| Self VISA Secured Credit Card | |

| No credit check |

Learn More >>> Read our full Self Financial review 👈

| Credit Strong Pros | Credit Strong Cons |

|---|---|

| Flexible loan options | $15 monthly fee |

| Reports to the major credit bureaus | No money upfront |

| No cancellation fee | |

| No credit check |

Learn More >>> Read our full Credit Strong Review 👈

Which Credit Builder is Better?

This comes down to your needs and situation.

Both products have easy qualification criteria, report to the three primary credit bureaus, and can be canceled at any time.

Credit Strong and Self have different loan amounts, monthly payment plans as well as loan terms to choose from. Credit Strong has credit builder loans with larger amounts and longer loan terms.

A longer loan term means more credit-building potential as you make more on-time payments. On the flipside, a shorter loan term means you get access to your savings sooner.

Both Credit Strong and Self offer 24-month loan terms, though Credit Strong also offers 36 and 48-month terms if you want to focus on building your credit over time.

Self also offers a secured VISA credit card that you are eligible for after you make three on-time payments and have paid at least $100 into your credit-builder account.

Both options have terms and features that may be appealing to you. Always take your personal situation and needs into account and make the choice that reflects your credit building needs.

Check Out Our Latest Credit Building Resources:

- Credit Builder Loans with Money Upfront 🥇

- How to Build Credit at 18 (Lifelong Strategies) 🥈

- Top Credit Builder Loans like Credit Strong 🥉

Need more than a few hundred dollars?

- Bigger loans, not tiny advances. Cash advance apps top out fast — PockBox helps you search personal loan offers that often start above $500.

- Any credit score welcome. Compare options from lenders that work with excellent, fair, and poor credit (approval and terms always depend on the lender).

- Free to shop around. Checking rates does not lock you into a loan — compare side by side, then decide.

- Borrow $200 From Cash App: How to Get Two Hundred Bucks With No Credit Check - July 21, 2026

- How to Borrow $50 Instantly (2026): Best Cash Advance Apps - March 31, 2026

- Borrow $50 Instantly in Canada (2026): Best Cash Advance Apps - August 5, 2025

- Results are not guaranteed. Other factors, including activity with your other creditors, may impact results. Failure to make monthly minimum payments by the payment due date each month may result in delinquent payment reporting to credit bureaus which may negatively impact your credit score. This product will not remove negative credit history from your credit report.